Unpaid super is no longer something directors can afford to treat as a minor payroll issue.

For many small business owners, superannuation still feels like something to deal with after wages, rent, suppliers and cash flow pressures. But legally and practically, super should be treated as part of the employee’s pay package — not something to catch up later.

From 1 July 2026, Payday Super requires employers to pay super at the same time as wages, fundamentally changing how super is calculated and managed.

This significantly reduces the margin for delay.

If an employer misses a super payment deadline, the issue does not simply disappear when the amount is later paid. Employers may become liable for the Super Guarantee Charge (SGC), which under the new framework is assessed much closer to each pay cycle.

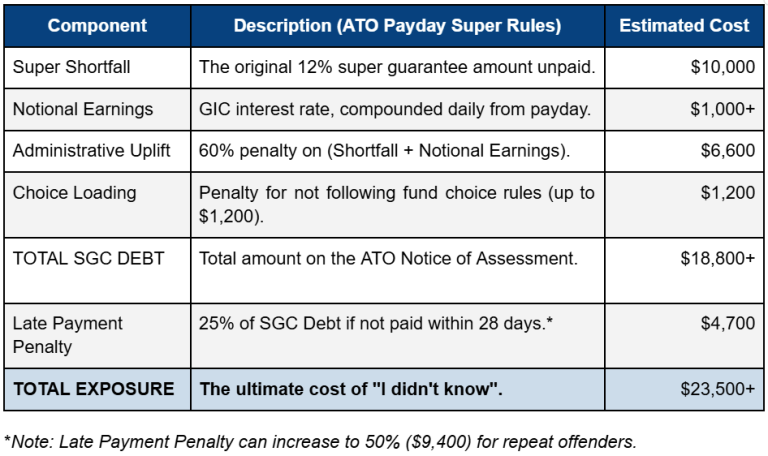

The SGC is expected to include:

Let’s say a business misses $10,000 of super and fails to deal with it properly.

That $10,000 may quickly become:

So a $10,000 super issue can quickly become a $20,000+ liability, even before ongoing interest and enforcement action are considered.

A $100,000 shortfall can move well into six-figure territory.

That is why unpaid super should never be treated as a small payroll delay.

Many directors underestimate the stakes.

Super is not just a company obligation. Under the Director Penalty Notice (DPN) regime, the ATO can make directors, including volunteer directors of not-for-profit organisations, personally liable for unpaid super guarantee obligations.

Without clear visibility over payroll and super, the risk can shift from the organisation to the individual.

The system itself has changed.

Under Payday Super, super obligations are no longer calculated and paid quarterly. Employers are required to pay super guarantee at the same time as salary and wages, with contributions needing to be received by the fund shortly after payday.

This removes much of the flexibility businesses previously relied on.

Quarterly habits are no longer sufficient.

Alongside operational and financial pressures, market behaviour is also shifting. After an extended period of cost-of-living pressure and inflation, consumers are becoming more cautious. Spending is increasingly focused on essential needs, while discretionary purchases are being delayed or reduced.

The cost of unpaid super is not just financial. It affects tax outcomes, cash flow, director exposure and employee trust.

In 2026, “I didn’t know” is not a position directors can rely on.

At Tailored Accounts, we help businesses review payroll compliance, identify late or unpaid super, and manage SGC obligations before they become bigger problems. With the move to Payday Super, now is the right time to strengthen your payroll process and reduce unnecessary risk.

Starting 1 July 2026, every Australian employer must pay superannuation (currently 12% of qualifying earnings) at the same time as wages. Contributions need to land in your employee’s super fund within 7 business days of each payday. No more quarterly super payments. No more breathing room.[1]

The amount you owe doesn’t change. But the timing does. And for many businesses, that timing shift is the whole problem.

Recent developments arising from the Middle East conflict are no longer just distant geopolitical events, but are increasingly reflected in the day-to-day operations of many organisations. The impact goes beyond fuel prices and logistics costs, extending into cash flow, financial forecasting, and how businesses make decisions in both the short and medium term.

Finding the right grant can feel overwhelming when you don’t know where to start, so we’ve pulled together a quick guide to some of the key funding programs available in 2026 for Canberra businesses.

Tailored Accounts © All rights reserved.

Liability limited by a scheme approved under Professional Standards Legislation.