Starting 1 July 2026, every Australian employer must pay superannuation (currently 12% of qualifying earnings) at the same time as wages. Contributions need to land in your employee’s super fund within 7 business days of each payday. No more quarterly super payments. No more breathing room.

The amount you owe doesn’t change. But the timing does. And for many businesses, that timing shift is the whole problem.

Under the current system, super builds up as a liability across the quarter and gets settled in one hit. That gap, sometimes spanning three to four months, has functioned as a de facto working capital buffer for many businesses — even though the funds were never theirs to deploy. From 1 July, that timing gap closes.

This matters because most small businesses don’t have much room to absorb it. RBA analysis of ABS firm-level data and bank liaison suggests that small business cash buffers have declined to pre-pandemic levels, with industries like hospitality holding thinner reserves than most. A 2025 CommBank survey found that nearly 80% of small businesses experienced cash flow difficulties in the prior twelve months, with 27 per cent dipping into personal savings or forgoing their own salary to keep things running.

Now layer on the debtor side. If your clients or funding bodies take 30 to 60 days to pay you, and many do, you’re already bridging a gap between when you pay staff and when revenue arrives. Payday Super adds super to the “pay staff” side of that equation, every single pay run.

The quarterly float is gone. Every pay cycle now needs to be fully funded — wages, PAYG, and super, all from current cash.

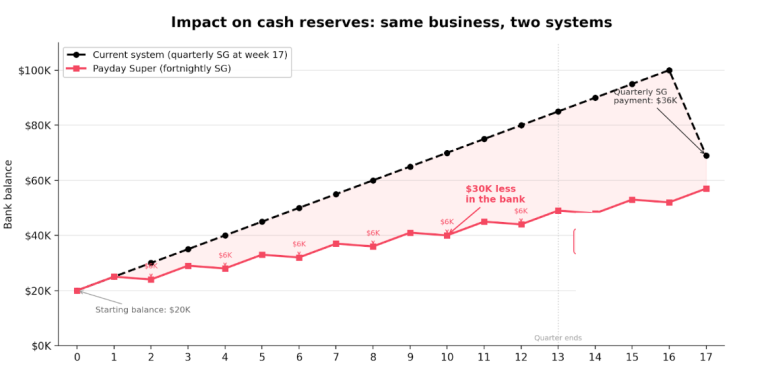

Take a small business with 10 employees on a fortnightly pay cycle, averaging $5,000 in qualifying earnings per employee per fortnight. The business brings in $5,000 per week in net cash (after wages, PAYG, and operating costs — but before super), and holds $20,000 in the bank.

no super leaves the business during the quarter. The bank balance grows steadily — $5,000 per week — reaching around $85,000 by week 13. The quarterly SG payment of $36,000 doesn’t hit until roughly week 17 (28 days after quarter end). The business absorbs it comfortably.

$6,000 in SG leaves the business every fortnight: weeks 2, 4, 6, 8, 10, and 12. The bank balance still grows, but more slowly. By week 10, the business has $30,000 less in the bank than it would under the old system. By week 12, the gap peaks at $36,000.

Both lines converge at week 17 — the total cost is identical. But the path matters. The Payday Super business has less cash on hand at every point during the quarter. A late-paying debtor, an unexpected expense, a slow fortnight — any of these hits harder when the buffer is thinner.

Weekly pay cycle: Super leaves every week (~$3,000), roughly 13 payments per quarter. The cash drain is steadier, and the administrative load is heavier.

Monthly pay cycle: Fewer payment events (3 per quarter), and the timing compression is less severe, but the float is still gone.

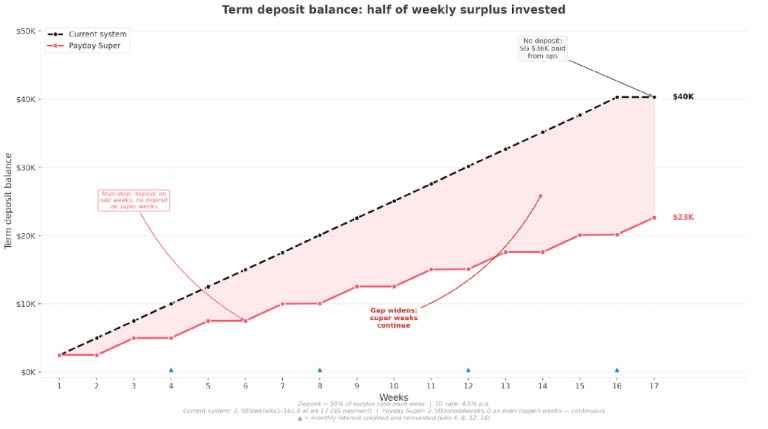

To illustrate, assume the business directs half of its weekly surplus cash into a 3-month business term deposit at around 4.5% p.a. The other half stays liquid in the operating account. Under the current system, a steady $5,000 weekly surplus means $2,500 flows into the TD every week. Under Payday Super, fortnightly super payments wipe out the surplus on every second week — meaning $0 goes into the TD on those weeks. Over 17 weeks, the difference in accumulated balances and earned interest is measurable.

Under the current system, every week produces a $5,000 surplus, so $2,500 goes into the TD each week. The TD pays interest monthly (credited at weeks 4, 8, 12 and 16), and credited interest is reinvested. The only disruption is week 17, when the $36,000 quarterly SG payment hits the operating account — no TD deposit that week.

Under Payday Super, super is paid every fortnight, continuously. On super weeks (2, 4, 6, 8, 10, 12, 14, 16), the $6,000 outflow exceeds the $5,000 inflow, leaving a $1,000 deficit and $0 available for the TD. On non-super weeks, the full $2,500 deposit proceeds. This creates the stair-step pattern visible in the chart below: rise on odd weeks, plateau on even (super) weeks — all the way through.

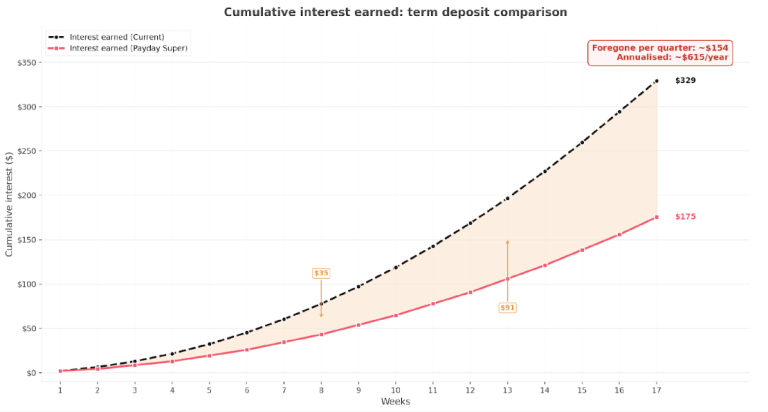

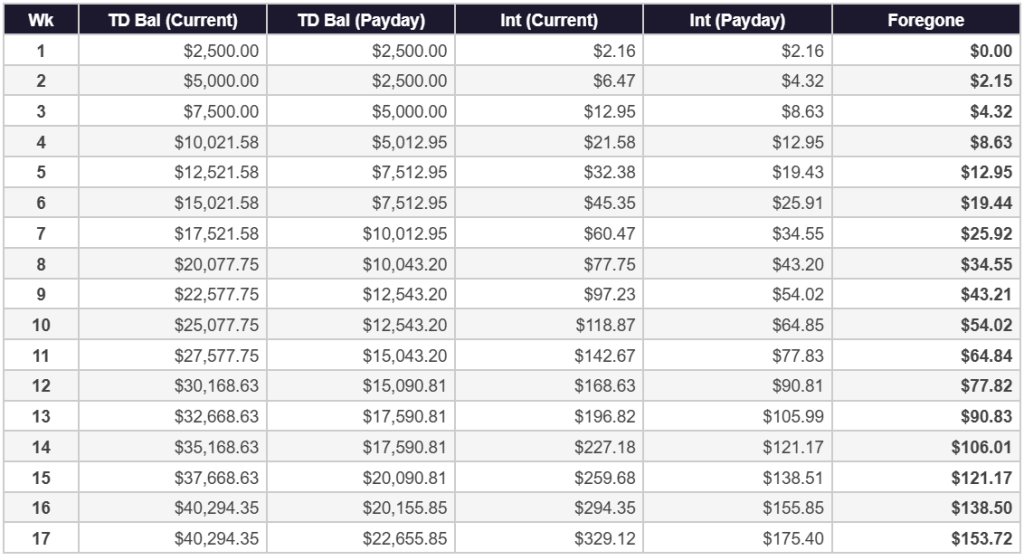

The table below shows the week-by-week term deposit balance and cumulative interest earned under each system. Interest is calculated as: TD balance × (4.5% ÷ 365) × 7. Credited interest (at weeks 4, 8, 12, 16) is reinvested into the TD balance.

Totals over the 17-week period:

For a 10-employee business, that’s modest. But it scales linearly with headcount. A 30-employee business on the same ratios loses approximately $1,845 per year. A 50-employee operation: over $3,075. Businesses that actively use short-term deposits, offset accounts, or cash management trusts to optimise returns on operating balances will feel it more.

Note: Payday Super pays $48,000 in super over 17 weeks (8 fortnightly payments) versus $36,000 under the current system (one quarterly lump sum). The Payday Super business is already settling obligations that extend into the next quarter, which is precisely the timing squeeze this reform introduces.

Payday Super permanently lowers the average cash balance the business holds across the year. That lower balance earns less interest and provides a thinner cushion. Unlike the SG expense itself, this lost interest income never comes back.

If the loss of the quarterly float leaves your business short, a few options are worth looking at before July. A business overdraft or revolving credit line can cover the fortnightly super payments without a new loan each cycle — talk to your bank about whether your existing facility is sized for the new timing. Invoice finance (also known as debtor finance) lets you draw against unpaid receivables, which matters most when your clients sit on 30–60 day terms and your payroll runs fortnightly. The Australian Small Business and Family Enterprise Ombudsman (ASBFEO) publishes guidance on working capital options and maintains a directory of support services. The government’s business.gov.au grants and programs finder can also surface state and federal assistance you may not be aware of, including concessional loan schemes and digital advisory programs.

For businesses with seasonal revenue or lumpy grant income, a short-term deposit ladder — staggering maturities across one, two and three months — can keep some funds earning interest while still freeing up cash each pay cycle. Match the structure of your cash management to the new cadence of your obligations. Quarterly-era assumptions about when cash needs to be available no longer hold.

Several features of Canberra’s business environment make this worse. Around 97% of Australian businesses are small (fewer than 20 employees). The ACT records both the nation’s highest insolvency rate and its lowest four-year business survival rate. In the Canberra Business Chamber’s mid-2025 Business Beat survey, only half of ACT businesses expected to make a profit, and 32 per cent reported not expecting to be profitable.

Many local SMEs are service providers to government: consultancies, IT firms, professional services, where payment terms can run 30 days or more. NFPs delivering government-funded programs face an even tighter squeeze. Grant funding often arrives on milestone schedules or in arrears, but payroll and super are due on a fixed cycle regardless.

If your business relies on government contracts or grant income, the loss of the quarterly super float removes one of the few timing buffers you had.

NFPs deserve a separate mention. Many run on grant funding with fixed disbursement schedules that don’t flex to match payroll timing. Your super obligations now follow your pay cycle, but your revenue follows a funder’s milestone schedule. That mismatch creates real liquidity pressure, especially for organisations with casual and part-time staff on award rosters. Allowances, penalty rates and back-pay adjustments all carry super obligations. And under Payday Super, the calculation base shifts from ordinary time earnings (OTE) to a broader concept called “qualifying earnings” (QE), which may pull in amounts not previously included in your SG calculations.

Boards and finance committees should treat Payday Super as a standing agenda item between now and July. The impact on cash reserves, going-concern assessments, and risk appetite needs to be understood at governance level, not only by the finance team

Late or underpaid super now attracts the Superannuation Guarantee Charge (SGC), a statutory charge comprising the shortfall amount, an interest component calculated using the general interest charge rate, and an administrative uplift. Unlike timely SG contributions, SGC amounts are not tax-deductible. The penalty cost sits entirely outside your deductible expense base. What was previously a minor timing issue correctable before the quarterly deadline can now become a compounding penalty within days.

The ATO will monitor compliance in near real time through Single Touch Payroll data. A transitional, risk-based approach applies for the first year (to 30 June 2027), but the legal obligation remains. Super must reach the fund within 7 business days. The transition period is for refining your processes, not for delaying them.

If you currently use the ATO’s free Small Business Superannuation Clearing House (SBSCH), it closes permanently on 1 July 2026. You’ll need to move to a commercial clearing house or a payroll-integrated solution, and you need to do it well before the deadline.

Super is only considered “paid” when it reaches the employee’s fund, not when it leaves your bank. Different clearing houses have different processing times — typically 2 to 5 business days — and that lag eats into your 7-day window. Choose your provider based on processing speed and payroll integration, not just cost.

Stop treating super as a quarterly line item. Build it into every pay run as a combined outflow alongside net wages and PAYG. Stress-test what happens if a major debtor pays late.

Transferring estimated wages, PAYG, and super into a ring fenced account each pay cycle prevents super from being absorbed by general trading expenses. It’s a simple discipline that eliminates one of the most common causes of accidental non-compliance.

If your clients take 45–60 days to pay but your payroll runs fortnightly, the cash flow gap just widened. This is the time to renegotiate payment terms, offer early-payment incentives, or tighten follow-up on overdue invoices.

If you carry a business overdraft or credit facility, the size of that facility was probably set based on quarterly super timing. It may no longer be adequate. A short conversation now is better than a shortfall in August.

If you’re on the SBSCH, select and test a commercial alternative now. Factor in processing times and ensure your internal payment deadline is set early enough — say, 3 business days after payday, to accommodate clearing house lag and still meet the 7-day window.

Artificial intelligence (AI) is becoming a helpful tool for accounting firms that want to save time and work more efficiently. It can assist with everyday tasks like drafting emails, summarising information and organising workflows – without needing major changes to existing systems. Here are nine simple, low-risk ways to start using AI to lighten the workload and free up time for higher-value work.

Finding the right grant can feel overwhelming when you don’t know where to start, so we’ve pulled together a quick guide to some of the key funding programs available in 2026 for Canberra businesses.

After a long break, coming back to work in January can make the pressure points stand out. It’s easier to identify the patterns: decisions that take too long, jobs that create constant interruptions, and weeks that fill up without moving the business forward.

A genuine reset is not about doing more. It is about clearing what is getting in the way, tightening your choices, and setting up the year to run with less strain.

Here are seven realistic ways to reset your business for the year ahead.

Tailored Accounts © All rights reserved.

Liability limited by a scheme approved under Professional Standards Legislation.